The Sunshine Interview: UHERO Economists Drill Down On Housing Policy

University of Hawaiʻi experts emphasized solving the state’s housing crisis requires building new housing because it frees up old housing as well.

May 17, 2026 · 31 min read

About the Author

Editor’s note: Civil Beat reporters and editors recently met with Carl Bonham, Steven Bond-Smith and Justin Tyndall of the University of Hawaiʻi Economic Research Organization. The focus was on recent UHERO reports authored by Bond-Smith, Tyndall and other economists on affordable housing and the Hawaiʻi housing market, and on the state’s stagnant economic growth.

The economists also discussed UHERO’s latest forecast for the state, which was released Friday. It reports that Hawaiʻi’s economy is facing “a new wave of uncertainty” as the war involving Iran drives up global oil prices that increases costs for consumers, raises travel expenses and slows growth in key visitor markets that support the local economy

This interview was edited for length and clarity and to allow some material to be used in other stories. Bonham began by discussing a recent gathering of UHERO professors and political leaders.

Bonham: We do a quarterly pau hana with all of our supporters and government officials, usually invite the mayors and the governor and they almost always come. It’s a closed-door thing. And the conversation can be really engaging at times. People (are) not too worried about what they’re saying in front of these people. And at the last pau hana Justin presented his (housing) filtering results. And I’ve got to say, this was probably the most engaging conversation that I’ve seen. And I won’t reveal who got the most heated, but there was a lot of excitement about it and an interest in making sure that the message, the research results, were widely distributed, because it’s an education piece.

Justin, your study was on The Central, a 512-unit condo that’s in the Ala Moana area. Tell us more about the report and your analysis of what you call the housing filtering process.

Tyndall: All of our conversations around housing in Hawaiʻi are almost exclusively around how we build new housing. We have like a hundred different rules on giving permission for developers to build housing. We have a lot of concern about what types of housing they’re building, where they’re building it. We spend years giving out permits and having public meetings on these debates. But one point is that only 3% of our housing has been built since 2010. So we’re maybe missing like 97% of the problem. And I think the issue is even more pronounced because brand new housing does tend to be more expensive.

So if our policy goal is to help lower-income people, 3% is even an overestimate. Most lower-income folks will never live in a brand-new housing unit. Most people circulate through the used housing market, either through renting or a resale market.

So I think a lot of our research at UHERO in the past around housing has been about the costs of regulation and why we don’t build more housing, and trying to put some numbers on the lost benefits from preventing new housing construction. This project is more about what happens when we actually do build housing. The idea was to do a deep dive into one building. Like you say, we looked at The Central.

How tall is that building?

It’s among the tallest in the state, and it’s in Ala Moana, connected to the mall almost. It’s like a 10-way tie because we have a 400-foot limit. The Central was built under the 201H (Development Assistance) program. Sixty percent of the units are set aside for income-restricted buyers. But the limit is pretty high for this program — up to 140% AMI. So a household earning $140,000 a year could qualify for one of these units. Some of the tranches are for lower income people.

The way we enabled this research was we purchased some data on address histories. We have this big data set, a national data set from a company that their main client is providing junk mail to people. Big companies would buy address data sets to send out targeted mailers.

This data, then, is telling you who is in there and how much they make and where they’re from?

Yes — importantly, where they’re from. We have it annually, so we can look at who exactly lives in all of the units in The Central and importantly, we can look at where they lived prior so we can link them to their prior addresses and we can say pretty explicitly where people came from.

There’s a couple of main findings. We have essentially data coverage for the whole country. So for people who lived in the U.S. prior, about 80% of them moved from other Hawaiʻi addresses. About 20% moved from mainland addresses. California is most represented. But we don’t find that this new condo is entirely occupied by out-of-state movers. The large majority is local people moving from other Hawaiʻi households. And the big policy upshot is that people who move into The Central then vacated their prior home.

So when we’re thinking about how we can create housing vacancies for people, even more important than the new units built in The Central were the vacated units from people who moved out of their prior address into The Central. We don’t have 100% data coverage, but our best estimate is we can find 500 local addresses that were vacated because people moved into The Central or because they vacated their home moving into the home of someone who moved into The Central. This is only in the first three years after The Central was completed. Over a longer term, we would expect to see this chain reaction of a lot more vacancies.

I think the other important finding is, on average, these vacated units were about 40% cheaper than the ones in The Central. So one criticism of The Central would be even the “affordable units” are relatively expensive and not attainable to a lot of people. But by building this tower, we liberated all of this other housing stock that is much more affordable. We see quite a few single family homes, diversity of neighborhoods, a lot of really old housing stock. We see some really low price point rentals and condominiums involved in these chains, sort of freeing up all of these opportunities for people to get into the housing market.

Most of the time we don’t allow new condominiums to be built, either because of the regulatory environment — they’re never considered in the first place — or ones that end up not getting through the regulatory process. But here’s one that did get through, and we find all of these benefits that sort of ripple through.

Bonham: That’s really the key — that if you don’t build new housing, you can’t free up the old housing. Affordable housing is old housing, period. The stuff that they’re targeting that we call affordable housing, it’s really middle-income housing. It’s not going to reach people below the middle income, and the only way you do that is by building enough units so that people who have the means can move up the ladder, if you will, move from an old place — you know, that one-bedroom, or that 600-square foot two-bedroom condo in Makiki that they’ve been living in for 30 years. Now that they have the income, they can move up and you’ve just freed up an affordable unit for someone else.

Is this an isolated case with The Central, or is this something legislators should be looking for, developers should be looking for going forward? We did a story some years ago on how most of those places in Kakaʻako are dark at night because a lot of people don’t actually live here.

Tyndall: We only looked at one building, but I don’t think there’s any strong case as to why this would be unique. I think one interesting thing about looking at this project was it’s 60% income restricted, 40% market, so we can look at both and compare them. We find both contribute to local housing supply.

Actually, we find the market rate units tend to free up more local housing units. More common for the income-restricted units is someone moved out of their parents house or with roommates or something and left behind a housing unit that still had people in it. So mom and dad, their kid turns 18 or something and moves into one of these income-restricted units, but mom and dad stay at home and they don’t create another housing vacancy. But with the market rate units, it’s almost exclusively entire families moving into these units, leaving behind the prior address.

And because we don’t have perfectly complete data, I can’t tell you exactly how many of the market rate units are empty. But we can get a good guess by the data we do have. So our estimate in the paper is about 10% of the units are probably vacant, which is about on par with just the state’s average vacancy rate according to the census. So it doesn’t suggest that these are just sitting empty as investment vehicles. We estimate the large majority are either owner occupied or rented out. There’s a lot of cases of foreign investors buying one of these units, but then we can observe someone living in it. So they’ve presumably rented it out to a local.

Steven Bond-Smith: It’s kind of evidence that granting an exception to allow higher density generates down that that moving chain. That’s pretty strong evidence for the additional building. Then I think we’re excited about the benefits of that exception, but I think it even just describes the benefits of building more in general, on any site. If you can build more, no matter there’s a quality of that supply, it generates supply down the moving chain for all levels of affordability.

Bonham: And an important piece about the “condos left dark” is that you really have to build at across the spectrum. If you don’t build a luxury condo that you can sell half of them to someone who doesn’t live here and they sit dark, then those people will find other pieces of property to buy. If they want to own property in Hawaiʻi, they can buy it. They can buy it in Waikīkī. They can buy a house in Mānoa and leave it empty half of the year. And so if you don’t build you’re going to create price pressures that spread throughout the economy because you didn’t build.

And if you don’t build, then the older units — there’s research nationally that has shown this — they get refurbished. Take the house I live in — it was built in the ’50s. When I moved in, I couldn’t get through the door to my bathroom unless I turned sideways, and the counters were all down below my waist. Fifteen years ago I looked for a place to move — an upgrade. I couldn’t find anything, and so we spent $100,000 to renovate. My neighbor moved out, and now it’s a rental. And sometimes it’s a rental with 10 people in it. That’s affordable housing. And if you don’t build something, the old stuff just goes up in value instead of filtering down and continuing to depreciate. I mean, the reason that it’s affordable is because it’s old. It’s not modern. It’s got single-wall construction, and the termites are holding it together.

This is the story that we hear from developers, business people — even I think the governor would say this is part of this whole initial housing policy — to just build a lot.

Bonham: This is a theory and there’s actually some decent evidence for it on the continent, but this is something that we’ve wanted to do for ages, and we weren’t able to do until we could buy the data. It took us a while to be able to. And admittedly, some of the people in the room, these are our supporters, so it’s their money that we’re using to buy the data. And so they were happy to see the evidence.

But it is interesting that you’re quantifying what you said, because as you pointed out, what we’re always seeing, and we see anecdotal evidence of it, is that when they build these buildings, a lot of the buyers are people from out of state, and because there is so much demand for Hawaiʻi.

Bond-Smith: Even if there is an out-of-state buyer, it is very expensive to just hold the property empty. So out-of-state investors can also rent out properties. And then that would be a lot of this as well. But people are moving in, and that frees up a home somewhere else someone can live in. And I would characterize the sort of filtering thing as being sort of two components. One is the moving chain that it creates when those units don’t sit vacant, and then the range of quality of housing that it frees up. And so it’s not just, even though you’re building a luxury unit, the person that’s moving is upgrading. So it’s creates a moving chain that frees up other supply. But that other supply is not at the luxury level.

Bonham: That other supply keeps getting cheaper and cheaper and cheaper the farther out you go.

Tyndall: There’s one example I use when I present (the paper). You can see an individual moving into one of the new units in The Central. She’s moving from an apartment built in the 1970s in this case, moving in with a roommate, leaving vacant this 1970s apartment, and then you can see someone moving into that unit from recovery development for people experiencing homelessness. With sort of two steps, we go from the new condo to someone finding housing who was sort of on the threshold of homelessness, and then presumably freeing up a bed in this recovery center.

This idea of the difference between affordable housing, as we call it, and housing that’s affordable — the housing that’s affordable is really the older housing. And you also said, “Well, this is really the only way build more.” Is it the only way? Is there a way to maintain the housing that’s affordable and prevent it from being redeveloped into affordable housing?

Bonham: One counter example to that is the example of my home, or anybody’s 1950s vintage single family home. You can’t prevent me from renovating it and turning it into an expensive piece of property. And one of the reasons that I do that is because there’s nothing new built. There are things you can do to try to preserve affordability, and we’re not suggesting that you shouldn’t do that. But we’re suggesting that if you’re going to grow the stock of units that are more affordable, you have to build housing — period.

We have a collaborative relationship with the (state) Department of Taxation. It’s actually in a (legislative) resolution from a couple of years ago, and we’re working on tax policy. But one thing that we would like to do — assuming that DoTax has time, because they work on the data, we don’t — what we’re doing right now is we’re looking at the value of the units that people are moving to and from, but if we can use tax data, we could potentially identify their actual incomes. Not at the individual level for the research. The theory is that it’s people of lower and lower income who are being housed in these moves, which is consistent with the fact that the values are pretty markedly lower.

Tyndall: Yeah, on per square foot basis, like 40% cheaper the ones that were vacated.

Is there anything specific to The Central that helped create that dynamic? Whether it was the percentage of income restricted units, whether it was where it was or there was other 201H project, anything that helped create that dynamic in a way that other projects haven’t or might not?

Tyndall: I think it was a pretty classic example of a new condominium development. It was under this 201H program. There’s a split between income-restricted and market rate units. But we see that in a lot of other projects.

Bonham: That’s probably the most predominant way that condo buildings are being built right now.

Tyndall: In Kakaʻako it’s a special development district, so there are a different set of rules, and some of those are able to give off-site affordable units. So they might be entirely market rate. I think it’s interesting to get to look at the difference between the filtering and the market rate and income-restricted ones. But we find they both are contributing to housing supply.

Bonham: One way that The Central maybe isn’t the best example is it’s on Oʻahu. You’re not going to put up a Central-sized tower in, say, Kahului or Hilo, but if you put up multi-unit, multifamily housing in one of those cities, we don’t know what the pattern would look like. We don’t know how many people from off island would buy in and certainly, if you put up a a tower in Kona or if you put it up on the west side of Maui, you’re likely to get more offshore buyers than, say, we do on Oʻahu. That doesn’t mean that the filtering doesn’t work. It’s just that the numbers would be different.

Tyndall: I think there’s an interesting life cycle to these buildings. I think if you just looked six months after completion, you might see quite a few of these units sitting empty because someone bought it as an investment, and they still haven’t got their act together. Maybe they’re planning to move here, or maybe rent it out, or something like this. But if you look at buildings that are 10 years old, maybe when they were finished they were seen as sort of like luxury market rate housing for offshore investors, but now they’re full or matching the local vacancy rate.

Does this kind of example make the case that the efforts to create affordable housing are less effective than just efforts to create more housing in general?

Tyndall: If we could, without cost, force housing to be more affordable, then that would be great. But the reality is, if you mandate units sell or rent at lower prices, the development is less profitable and we get less development. So this research suggests it’s really a numbers game. We need to build a lot more housing units. So policies that prevent that from happening by making development really expensive, including inclusionary zoning policies, are probably counterproductive in addressing market rate housing.

Bond-Smith: The caveat on that is that they get an exception to the amount that they can build. So by getting that, by having that 60% caveat, they can build twice as many units. That’s what really generates that sort of cross subsidy to those affordable units. They’re allowed to build extra buildings which they wouldn’t have otherwise been allowed to build. That, in itself, creates some extra units.

Bonham: The problem is, we’re measuring the wrong thing. I remember a particular politician being interviewed, and maybe it was even by Civil Beat, about what they were really proud of. And they said, “Well, we built 3,000 affordable units.” And I thought, “Okay, now let’s go look at the affordability statistics. Yeah, they haven’t budged. People are still paying a large share of their income for rent. It hasn’t budged. So we’re measuring the wrong thing, and the total number that period wasn’t much higher either.

I wonder if we might segue a little bit. I do want to talk about our stagnating economy and how it’s not so much Hawaiʻi’s high cost of living that’s a problem so much as it is limited opportunities here. Steven, you’ve written about how more residents have left Hawaiʻi than have come here from the continent over the last 23 out of 25 years. Everyone says it’s the cost of living, but in fact, your research shows it’s really a dominant industry, tourism, a stagnant economy, low wages. I don’t know that we’ve really recovered, at least as it says in one of your pieces, since the Japanese bubble of the 1990s.

Bond-Smith: What that piece was looking at was, when you compare Hawaiʻi with the rest of the United States, we should really adjust for our cost of living. And once you adjust for cost of living, you can then be comparing on sort of a like-for-like basis. We’re comparing on the same prices at that point. And the main thing that you see is that Hawaiʻi has always been expensive, so the cost of living in Hawaiʻi is a problem. But it was also a problem in 1960 and 1970 and 1980, and at that time people weren’t leaving. People were coming to Hawaiʻi because they had incomes that were also 20% higher than the continent, and they could afford that additional margin.

Now, once you adjust for cost of living, their effective income was a little bit lower than the continent, or the effect of GDP if their their jobs (income) was a little bit lower. But that also didn’t matter. You’re willing to pay it to live here. That was small. It was relative. It was closing over time. It was reducing over time, because Hawaiʻi was growing faster than the continent. And that was the price of paradise. And it stayed relatively constant right up until 1990 when we had the “Lost Decade” (a long period of economic stagnation triggered by the collapse of a massive asset bubble).

So where’s that gap today?

Bond-Smith: We had this last decade where with decline in growth, and then there was a recovery post-Lost Decade of the early 2000s. So I just captured that as a whole period — what’s the real growth over that time, adjusting for cost of living, and then also looked at the period since 2005 until today, also adjusting for cost of living, and the total amount of the annual growth across that time is the same basically as the last decade. And it’s early recovery in the early 2000s is effectively the same as what we’ve had in the subsequent period.

This is your writing from a February paper: “Hawaiʻi increasingly resembles regions that are well recognized to have fallen behind.”

Bond-Smith: Yeah. So in making these comparisons, I then also made the comparisons with other states too. I adjust their cost of living, I look at average incomes, or GDP in West Virginia, Mississippi …

Economically distressed areas.

Bond-Smith: These places that have lower incomes in the U.S. typically also have lower cost of living. It’s really cheap to rent a house in West Virginia. So your cost of living is 10% to 15% lower than it is to live in the U.S. on average, whereas in Hawaiʻi it’s 10% to 15% higher. You make those adjustments to incomes in those places. Actually the real income on average for Hawaiʻi is about the same as West Virginia, Louisiana or Mississippi. And so the effective value, the real value of a job in Hawaiʻi is about the same as some of these places known as being economically distressed.

But the real cause of this is this long run, slow growth that we’ve had since the early’ 90s. It’s not that Hawaiʻi suddenly got more expensive over that time. Hawaiʻi was already expensive in the ’60s and ’70s. The trajectory changed around 1990. It’s not that Hawaiʻi didn’t recover from the Lost Decade. It’s just that its long-run trajectory dropped, and that long-run trajectory has stayed the same, and we’re still on that level. But that means the gap gets wider and wider and wider. So even though that gap had virtually closed in 1990, that gap is now three or four times the size.

So the answer to that dilemma is to, what, increase growth, lifting productivity?

Bond-Smith: The point in my report was that we can focus on cost of living. Cost of living is a big problem. But let’s say we solve the cost of living problem. We made it that the cost of living in Hawaiʻi is the same as the cost of living on the continent. That’s a one-off step change. It doesn’t change what that trajectory is. All it does is kick the can down the road that in 20, 30 years time, if we carry on that trajectory, that gap widens to where it is now again.

So the only way to really solve that is to change that trajectory, to lift productivity growth that our economy is growing, rather than the relatively slow, stagnant growth that we’ve had.

How do you see being able to do that? This has been studied before.

Bond-Smith: The main things that came up were in fishing and aquaculture cluster and a water-transportation cluster, which includes freight and ship building, boat building and so on. But I don’t know what’s wrong, why there isn’t more aquaculture here, or why there isn’t more commercial fishing.

Bonham: You can almost bet on regulation as being high for some of these things.

Bond-Smith: It’s always certainly regulation and other things, it’s going to be some infrastructure. For other things, it’s going to be something else.

These things, aquaculture and even water carriers, we’ve been talking about for decades as well.

Bond-Smith: Yeah, and that also made sense, the things that I found, totally driven by the data, were the same things that everyone would be talking about already, but still not found good solutions. And so my real conclusion from that was that it’s not so much what we move into that’s important, it’s really how we get there. We need to create, in my view, a policy mechanism for addressing barriers to new businesses or new industries, or barriers to growth in general.

Bonham: The bottom line is that business as usual isn’t working. It hasn’t worked and it’s not working. So we’re talking, both in housing and in economic development, about ways to change that, and one of them is that once you’ve identified what the barriers are, and you have a proposal for how to fix them, and it’s industry wide or not company specific, then you have to actually follow your results, measure the outcomes and change if it’s not working. We can’t wait 10 years to find out that this investment was a total failure, or this change in regulation isn’t enough. We have to monitor it and be completely willing to fail too.

Bond-Smith: Doing nothing really isn’t an option. We’ve got to do something. Let’s put out a portfolio of things that we can do. And we’re going to get it wrong. Accept that we’re going to get it wrong a bunch of times, but then also have this layer of monitoring and adaptation and governance. That means that for the things that are going really wrong, we can can them before they become too expensive. For the things that are not working perfectly, maybe we just need to make certain adjustments. Maybe there are some things that are actually working well and we’re just not measuring the success properly.

But this constant monitoring and adaptation of those sorts of initiatives, and ultimately canning the ones that are too costly and aren’t working would lead to then a set of initiatives that do work, because we have to do something.

What you’re describing is what I would say is a real paradigm shift, a very dramatic overhaul of the way we are doing things.

Bonham: The short answer is “yes.”

Bond-Smith: For growth initiatives, we could be talking about permitting. Permitting time should have a certain amount of time that we can aim for and say it’s successful. If we have 80% of permits passed in a certain period, and if they’re not hitting that, then there can be consequences for that or we need to adapt what the processes are.

Bonham: You can come up with 20 examples of economic development policy that the state has put in place over the last 50 years — okay, I’m making the numbers up again. But you can come up with many examples where 10 years later, there’s a story in the Star-Advertiser or Civil Beat that says, “Gosh, we threw a whole bunch of money at this, and right now, no one knows what happened to it.”

I’m thinking of the Act 221 high-tech tax credits over 20 years ago.

Bonham: We wrote about that extensively back in the day.

A lot of times people perceive it sometimes not as a broad policy change that’s needed to affect everybody in the community, but something to support businesses, which they see is bad. How do have you propose overcoming that perception?

Bonham: How do you communicate this to the public, that this isn’t just about, “Oh, we need to grow faster and businesses need to change things for businesses,” because it’s not for businesses. And in my mind, it’s kind of like Justin’s chart that shows someone moving out of a homeless recovery shelter into a building. Here we’re talking about people’s incomes actually being able to go up fast enough so they can afford to live here. It’s really about whether or not your kids get to live in Hawaiʻi.

Bond-Smith: It’s also that when people are looking at their incomes, it’s not just that they find Hawaiʻi expensive. They might be able to afford to live here because they have an education and a good income, and they can afford to live here if they really stretch. But they can get a house that’s 50% larger in Las Vegas without a mortgage because they’ve already saved that much. That’s really what pulls people away, but that also pulls the incomes away for other people on that level as well. There is this societal mix that it’s not just even the people that find it really distressing and unaffordable, but right across the income spectrum. The pull to the continent is what that gap is doing.

I wonder if we might conclude by bringing up the current economic outlook.

Bonham: The bottom line in this environment is no one knows what the world’s going to look like tomorrow or next week or next month, because no one has a clue how the Iranians and this administration are going to resolve the situation, how long it’s going to last. We don’t even know how much damage has actually been done to the energy infrastructure in the Persian Gulf region.

And so that baseline still has oil prices elevated — I think we end the year at about $85 a barrel on Brent in the baseline scenario. We actually think of the baseline scenarios maybe about as almost the best case scenario at this point, because we’re thinking about the strait being closed completely the rest of this month and then reopening.

In our pessimistic scenario, think about the straight being closed until end of July. I think oil price spikes to $100 in the second quarter. I think we have Brent at $165 a barrel, and I think it’s still at $125 at the end of the year, if I remember correctly.

So then, what do those do to Hawaiʻi economy? Well, first and foremost, they raise our inflation. In our baseline scenario, I think inflation jumps to about 4% in 2025. Really pretty manageable, roughly 100 basis points more inflation than we would have thought about in our last forecast. And then in the pessimistic (scenario) you’re talking about 5% inflation, so not just 1% more, 2% more.

And in the baseline forecast, we’re talking about losing visitors. Basically, we started off the year relatively strong, even with the Kona storms. And then in our baseline, basically, arrivals continue to decline for the rest of the year from that high peak, and we end up losing about a little bit less than a billion dollars in real visitor spending in 2026.

It’s actually not quite as bad as the aftermath of the Maui wildfires. I think we lost about a billion dollars in visitor spending because of people not going to Maui, the high-spending destination. And here we’re talking about losing $800 million because some visitors stay away.

So the pessimistic scenario really is a recession scenario. It’s a global recession scenario. It’s that kind of oil price shock.

We’ve probably lost close to a billion barrels of oil and we haven’t reduced demand. We’re reducing inventories, but not by that much. So if this goes on another four weeks, another six weeks, then those inventories become crisis level, and the prices go up that much, because they have to destroy demand. They have they to go up enough so that people stop driving, they turn off their air conditioners, factories shut down in other parts of the world. It’s not in the U.S., although prices will go up and destroy some demand. But there’s not going to be shortages in the continent of the U.S., outside of maybe the West Coast, which gets so much of its refined product and some of its petroleum from Asia.

Bonham: So look at this as a tax increase. This is basically a tax increase brought to us by this administration and the Iranians and that’s for everybody who is now putting gas in their car at $4.50 a gallon on average on the continent or much more in Hawaiʻi. That’s money that they don’t have to spend on eating out. They have to think twice about a vacation to Hawaiʻi. And that’s just gasoline. It doesn’t count all the other things. So it’s not pretty. There is no way to put a positive spin on any of this.

Bond-Smith: Another point I would make is that Hawaiʻi is particularly sensitive to shocks that affect tourism numbers because of its dominance of tourism, and the combination of people having less disposable income just because prices are going to go up across the board and everything’s using energy and they’re paying more for gasoline for their car cuts out their disposable income. Plus the cost of their vacation becomes more expensive. That compounds the shock that gets built in Hawaiʻi.

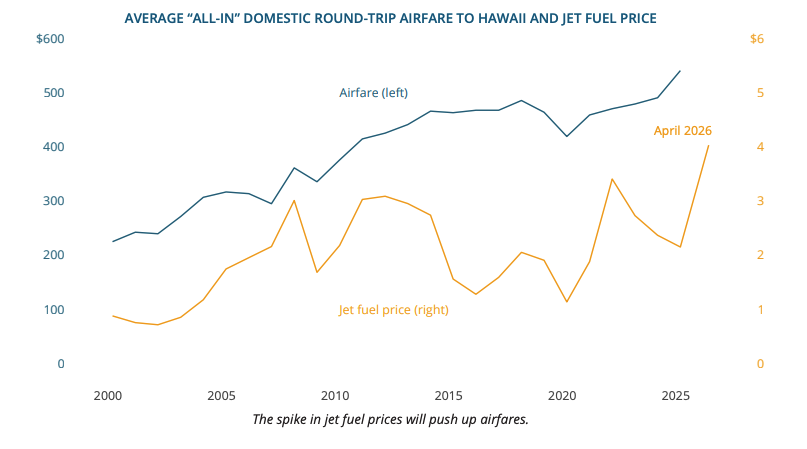

Bonham: The interesting thing right now is that you’re seeing almost none of this in any of the most recent best data we have. If you look at the airline seats outlook that DBEDT publishes, it shows almost no change in the seats outlook all the way through June. You’re seeing some decline in international seats, but the U.S. carriers have shown almost no reduction in air seats. So now their costs haven’t gone up that much yet. What you’re seeing is air carriers are increasing fees for checked luggage, and you got to pay 50 bucks to pick your seat, or something like that.

So one place where you could see some real problems is if the airlines start cutting routes. So if you don’t live in L.A., you might not be able to get to L.A. to get on your flight to Hawaiʻi. But right now, none of it’s really showing up in the data in a meaningful way.

Okay, but it sounds like you’re suggesting it’s going to.

Bonham: We think it’s going to, yes.

Bond-Smith: And there’s a greater risk for Hawaiʻi.

Sign up for our FREE morning newsletter and face each day more informed.

Sign up for our FREE morning newsletter and face each day more informed.

Local reporting when you need it most

Support timely, accurate, independent journalism.

Honolulu Civil Beat is a nonprofit organization, and your donation helps us produce local reporting that serves all of Hawaii.

ContributeAbout the Author